As former Senator Max Baucus once observed, “tax complexity itself is a kind of tax.” While this is the case every year, this is especially true in 2026 as many significant tax policy changes create new tax and financial planning opportunities. From new restrictions on retirement catch-up contributions to expanded deduction limits, understanding these tax law changes is essential for making informed decisions in the coming year.

For many investors, particularly those over the age of 50 with higher incomes, these changes require careful planning at the start of the year. Rather than viewing tax policy shifts as individual changes, informed investors can view them as opportunities to refine their strategies and strengthen their long-term plans.

Catch-up contributions face new Roth requirements

One of the most significant changes affecting retirement savers for tax year 2026 involves catch-up contributions. For years, employees aged 50 and older have been able to contribute beyond standard limits in order to boost their retirement savings. This is valuable for individuals in many situations, such as those who started saving late, need more to retire, or faced financial setbacks earlier in their careers.

One of the most significant changes affecting retirement savers for tax year 2026 involves catch-up contributions. For years, employees aged 50 and older have been able to contribute beyond standard limits in order to boost their retirement savings. This is valuable for individuals in many situations, such as those who started saving late, need more to retire, or faced financial setbacks earlier in their careers.

Traditionally, investors have had flexibility in choosing between pre-tax and after-tax (Roth) options. Starting in 2026, however, high earners face a new restriction. Employees with Federal Insurance Contributions Act (FICA) wages of $150,000 or more must now make all catch-up contributions as Roth contributions. This means that these funds are invested after taxes, but will still grow and can be withdrawn tax-free in retirement. The standard catch-up amount has increased by $500 to $8,000 for those 50 years and older, while the “super catch-up” for those aged 60-63 remains at $11,250.

Why does this matter? For high earners who previously relied on pre-tax catch-up contributions to lower their current tax bills, this change could mean higher taxable income today. For example, a 55-year-old earning $150,000 in annual income who previously would have made a $7,500 pre-tax catch-up contribution would have reduced their taxable income by $7,500. Now, that same contribution must be made after-tax, increasing their current year tax liability.

So, while Roth contributions offer benefits such as tax-free growth and withdrawals in retirement, they provide no immediate tax relief. For those in their peak earning years who are counting on catch-up contributions to manage their current tax burden, it’s important to evaluate how this change affects their tax planning strategies.

The SALT deduction cap has been raised significantly

Another major change is expanding opportunities for many taxpayers. The state and local tax (SALT) deduction has been a central issue in tax policy for years, affecting millions of Americans who pay significant state and local income, property, and sales taxes. The SALT deduction allows taxpayers to reduce their federal taxable income by the amount they pay in state and local taxes, effectively preventing taxation at multiple government levels on the same income.

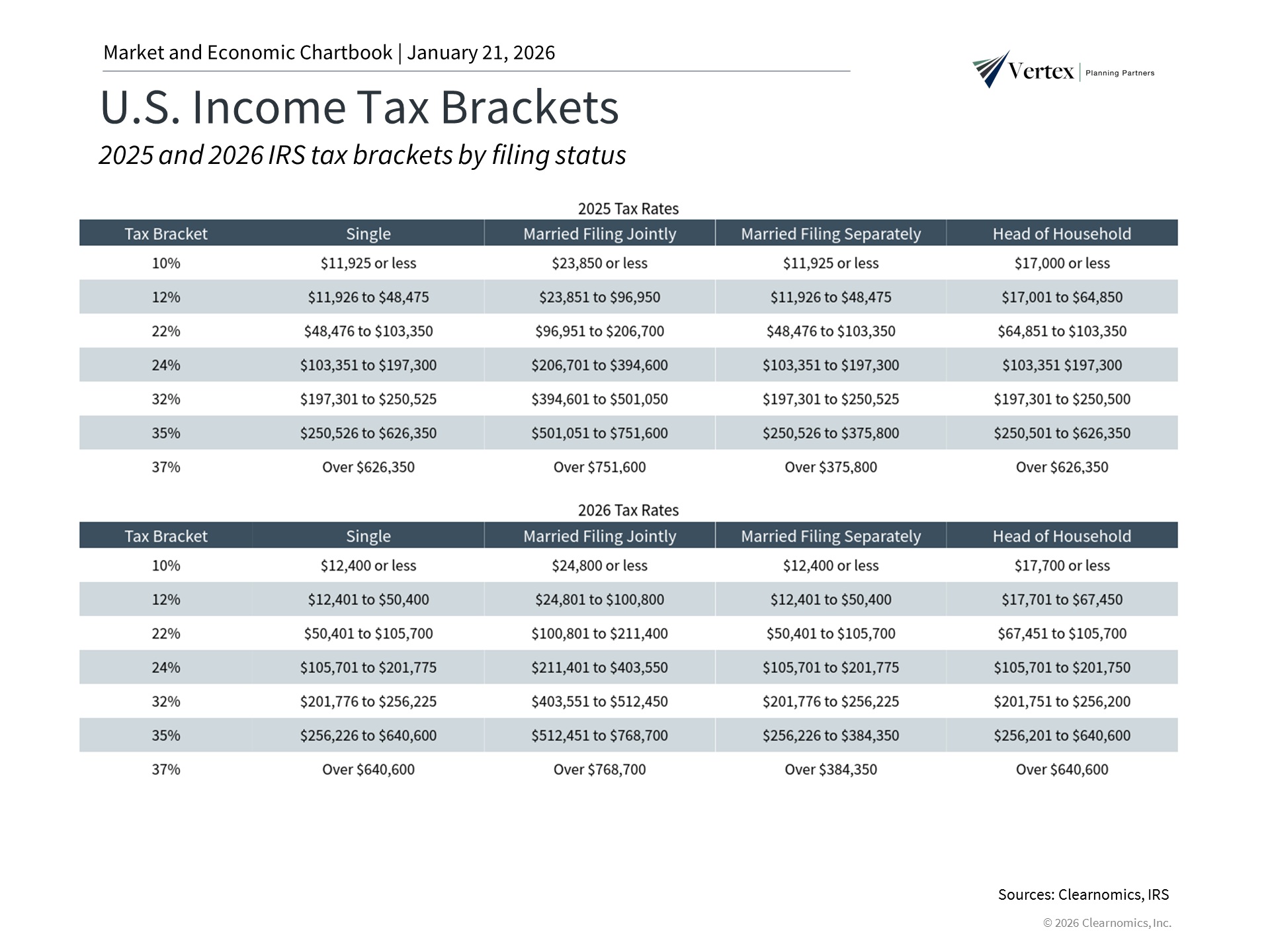

The SALT deduction, which had been capped at $10,000 since the Tax Cuts and Jobs Act of 2017, has now been raised to $40,000 for tax year 2025 and $40,400 for tax year 2026, and increases annually by 1% through 2029 by the One Big Beautiful Bill Act (OBBBA). This change affects many Americans, but is particularly significant for residents of high-tax states like California, New York, and New Jersey, where state and local taxes can easily exceed the previous $10,000 cap.

Importantly, the higher limit makes itemizing deductions more accessible for many households who have been taking the standard deduction since 2017. To understand why this matters, it helps to know how the tax calculation works. Taxpayers can choose between taking the standard deduction or itemizing their deductions. The standard deduction for 2026 is $16,100 for single filers and $32,200 for married couples filing jointly. Itemized deductions include things like mortgage interest, charitable contributions, medical expenses above a certain threshold, and state and local taxes.

When the SALT cap was set at $10,000 in 2017, it dramatically reduced the benefit of itemizing for many households. Combined with the doubling of the standard deduction at that time, the percentage of taxpayers who itemized fell from about 30% before 2017 to just 10% in 2022 according to the Tax Policy Center.1 Now, with the SALT cap raised to $40,400 in tax year 2026, many more households may find that itemizing saves them money.

As a simplified example, consider a married couple in California with $35,000 in state and local income tax, $8,000 in charitable giving, and $12,000 in mortgage interest. Under the old $10,000 SALT cap, their total itemized deductions would be $30,000 ($10,000 SALT cap + their other deductions). Since this falls short of the $32,200 standard deduction, this couple would not choose to itemize. Under the new 2026 rules, they can deduct the full $35,000 in state and local taxes, bringing their itemized deductions to $55,000 which reduces their taxable income by an additional $22,800.

The real complexity of tax planning isn’t just understanding each change in isolation, but also how they affect your entire financial picture. This becomes even more complex for retirees navigating Social Security.

For instance, the income thresholds that determine how much of your Social Security benefits are taxable haven’t changed in decades. This means that any changes that increase your Adjusted Gross Income (AGI), such as the new Roth catch-up contribution rules, may cause more of your Social Security benefits to become taxable.

It’s important to note that there is also a new “senior bonus” deduction available for the 2025 to 2028 tax years for those aged 65 and older. This is an additional $6,000 deduction for single filers or $12,000 for married couples, even if you itemize. However, this phases out for modified AGIs between $75,000 and $175,000 for single filers and between $150,000 and $250,000 for married joint filers. This adds more complexity since decisions that increase your AGI could also reduce or eliminate this deduction.

The expanded SALT deduction also creates strategic opportunities, particularly for those who previously took the standard deduction. If you’re now close to the itemizing threshold, you might consider strategies such as bunching charitable contributions into a single year, prepaying property taxes where allowed, or timing other deductible expenses to maximize the benefit. Of course, any specific strategy will depend on your particular circumstances. However, it’s important to remember that the increased SALT cap is temporary and scheduled to revert to $10,000 in 2030, creating a window of opportunity to take advantage of higher deductions while they’re available.

The bottom line?

The tax landscape for 2026 is complex with multiple moving parts that affect households differently. Viewing these holistically, and planning accordingly, can increase the likelihood of financial success.

Here are other articles on Tax Planning >

References

1. https://taxpolicycenter.org/briefing-book/what-are-itemized-deductions-and-who-claims-them

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly.

All investing involves risk, including loss of principal. No strategy assures success or protects against loss. The economic forecasts set forth in this material may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.